There’s a joke about a CEO who gets a quarterly profit and loss statement showing his company is losing money. “That’s impossible,” he says to the CFO, “all five divisions reported they were profitable this quarter.”

CPA humor. There’s nothing like it.

How could all five divisions make a profit while the company shows a loss? In a word: overhead. Each division is probably calculating its profits without deducting an appropriate share of the company’s overhead expenses.

This is not just a problem for accountants and CEOs. Litigators have to deal with this issue when there is a claim for lost profits damages. Any time a plaintiff tries to calculate lost profits—with or without help from an expert—there is the thorny issue of overhead.

A decision from the Fifth Circuit Court of Appeals shows how important this issue can be. In Motion Medical Technologies v. Thermotek, the Fifth Circuit reversed a jury’s award of over $1.5 million in fraud damages because the award was based on evidence of gross profits, not net profits.[1]

Why? Gross profits don’t account for the company’s overhead, while net profits do. The plaintiff had only offered evidence of gross profits, and Texas law requires evidence of net profits.

Simple in theory, but not so simple in practice. Let’s take a closer look.

An accounting lesson from a litigator

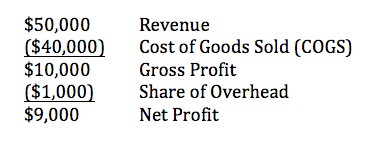

To illustrate, let’s take my favorite hypothetical company, Paula Payne Windows. Paula Payne buys windows from manufacturers and sells them to its customers.

*WARNING* I have no background in accounting, other than litigating cases with accounting issues, so you could say I know just enough accounting to be dangerous. But here we go.

Paula Payne’s revenue is what the customer pays Paula Payne for the windows. Paula Payne’s cost of goods sold (COGS) is what it pays the manufacturer plus the cost of shipping. Revenue minus COGS is gross margin, or gross profit. Gross profit minus overhead is net profit.

So, Paula Payne’s oversimplified P&L for a big window sale looks like this:

Yeah, I know, there’s also stuff like interest, taxes, depreciation, etc. That’s why I say oversimplified.

Plus, there’s usually some wiggle room in each line. For example, it’s clear that the money Paula Payne pays the trucking company to deliver the windows is part of COGS, but what about the lady in the office who talks to the trucking companies on the phone all day? Is her salary part of overhead or COGS?

Then there is the question of allocation. What share of Paula Payne’s total overhead should it allocate to one particular sale, or group of sales?

You may be thinking that’s what an accounting expert is for. We’ll just ask a CPA how to allocate overhead based on Generally Accepted Accounting Principles (GAAP), right?

The problem, I’ve learned, is that GAAP doesn’t really care how you allocate expenses for any particular transaction. GAAP deals with “financial accounting,” which is how you get to the P&L statement the company provides to the outside world. GAAP wants to make sure that all expenses are deducted before you get to the bottom line. It doesn’t really care how the company slices and dices those expenses internally.

That’s “management accounting,” which is not governed by GAAP. If a company wants to figure out internally how much net profit it makes on a particular transaction, it can use pretty much any reasonable method it wants.

*Update: Some accountants tell me the right way to allocate overhead expenses is to distinguish between variable and fixed. To determine net profit, you deduct the variable expenses, i.e. the ones that rise and fall with changes in sales volume, not the fixed ones. You can look historically at the company’s P&Ls to see which are variable vs. fixed.

But my accountant readers (I have at least two) are probably cringing at my explanation by now, so let’s get to something I know better: litigation.

How not to calculate lost profits in litigation

In Motion Medical, ThermoTek sold a medical device called the “VascuTherm” system. Orthoflex, a rival company, allegedly misappropriated information about Thermotek’s device and started selling its own knockoff device. ThermoTek sued Orthoflex for unfair competition and fraud.

The unfair competition claim was preempted by federal copyright and patent law.[2] That’s an important issue in its own right, but I’ll leave it to a smarter IP lawyer to blog about that. Let’s focus on the damages for the fraud claim.

ThermoTek’s expert witness testified that he used ThermoTek’s gross profit margin, meaning gross sales minus cost of goods sold, to calculate lost profits. He determined total lost profits for lost sales of the VascuTherm system by multiplying average monthly sales by unit sales price and relevant time period, and then deducting cost of goods sold.

“But that is the very definition of gross profits,” the Fifth Circuit scolded. “Indeed,” the court said, “the expert himself conceded on cross-examination that his numbers reflected ‘gross profits rather than net profits.'” The expert also acknowledged “his margins were high because they did not account for ThermoTek’s other business expenses.”[3]

The problem for the plaintiff was that Texas law requires the plaintiff to prove net profits, measured by the plaintiff’s total receipts minus all expenses incurred in carrying on the business. So, in the words of Willie Wonka, “You get nothing! You lose! Good day, sir!”

But surely it wasn’t that simple, right?

Well, it turns out there are some exceptions. First, for certain intellectual property claims, the plaintiff can seek an “accounting” of lost profits, where the plaintiff only has to offer evidence of its gross profits, and the burden is on the defendant to prove any costs that should be deducted to get to net profits. But ThermoTek’s common-law fraud claim was not such a claim.

Second, the court acknowledged that a plaintiff’s failure to include overhead expenses in the calculation of lost profits is “not fatal” if, for example, there is evidence the plaintiff was already profitable when the damages began and could have made the lost sales using only its existing resources.[4] But that argument, Judge Higginson wrote for the court, was not made by ThermoTek or supported by the trial record.

Perhaps this part of the opinion points to a solution for plaintiffs. Imagine ThermoTek’s expert had simply testified, “I didn’t deduct any overhead because ThermoTek was already profitable when the lost sales started, and my investigation satisfied me that ThermoTek could have made those additional sales without any increase in its overhead.” Would the gross profits award then be affirmed?

Lessons for litigators from Motion Medical

That last question points to some lessons litigators—and their hired experts—can learn about lost profits damages from Motion Medical.

If you represent the plaintiff, work with your damages expert early on to decide whether to calculate lost profits based on gross profits or net profits. The safer course, of course, is to go with net profits. In that case, the tricky part is figuring out what percentage of the plaintiff’s overhead to allocate to the lost sales. But as long as the expert uses some reasonable method of allocation, you should be ok.

On the other hand, safer isn’t always better. Net profits may undercompensate your client. If the plaintiff company was already profitable, and if you can make a credible argument that the company would have made the additional sales without any increase in its overhead, you may want to be more aggressive and go for gross profits, relying on the second exception cited in Motion Medical. But be careful. Make sure you offer evidence to support those assumptions, and prepare your expert to explain why overhead was not deducted.

If you represent the defendant, you have some strategic choices to make if the plaintiff presents a damage theory based on gross profits.

First, for the defense there is always the dilemma of whether to designate a damages expert at all. You worry that presenting an expert to calculate the plaintiff’s damages implies that your client did something wrong and that the plaintiff was, in fact, damaged. Often you would rather just attack flaws in the plaintiff’s calculation.

On the other hand, if the plaintiff’s expert offers an inflated lost profits calculation, and you offer nothing, you may get stuck with the plaintiff’s number.

The second decision is when to attack a calculation of gross profits that you think is defective. If you’re working hard to settle the case, you may want to press the issue earlier, e.g. hammering on it at mediation.

But generally I prefer to wait until trial, when it is usually too late for the plaintiff to fix a defective damage calculation. If I represent the defendant, it’s not my job to tell the plaintiff how to do a proper lost profits calculation.

Or is it?

Is it unprofessional to wait until trial to attack a gross profits calculation?

On at least two occasions I waited until trial to argue that the plaintiff’s damage calculation was defective because it didn’t deduct all the necessary expenses. It did not make me popular with opposing counsel.

In one case, I sent interrogatories to the plaintiff asking about its calculation of damages. The plaintiff responded with a calculation that was obviously based on lost revenues, not lost profits. I sat back and waited.

Then, less than 30 days before trial, plaintiff’s lawyers realized they had a problem and tried to cure it with a new calculation that included expenses. I objected. Strenuously. The judge said sorry plaintiff, you don’t get to offer any evidence of damages. Opposing counsel was livid.

In another case, the plaintiff offered evidence of the profits my client made from its alleged wrongdoing, without deducting any overhead. When the president of my client took the stand, I asked “what is your monthly overhead?” You’d think I had kicked an anthill. The defense lawyers practically jumped up and down complaining “he didn’t produce any documents showing overhead!”

My response: “you didn’t ask for them.” Objection overruled.

In both cases, the plaintiff’s lawyers kind of took it personally. They were pretty angry with me. Now, when someone gets really angry with you, there’s a part of you that instinctively feels a little guilty, like maybe you did something wrong (unless you are a sociopath).

So it made me wonder, was it unprofessional of me not to warn them that I was going to attack their defective damage theories? In the first case, should I have relented and said, “ok, it’s no big deal, you can offer your revised calculation”? In the second case, should I have provided information on my client’s overhead in advance?

Tell me what you think.

___________________

Zach Wolfe (zach@zachwolfelaw.com) is a Texas trial lawyer who handles non-compete and trade secret litigation at his firm Zach Wolfe Law Firm. Thomson Reuters named him a Texas “Super Lawyer”® for Business Litigation in 2020, 2021, and 2022.

Zach Wolfe (zach@zachwolfelaw.com) is a Texas trial lawyer who handles non-compete and trade secret litigation at his firm Zach Wolfe Law Firm. Thomson Reuters named him a Texas “Super Lawyer”® for Business Litigation in 2020, 2021, and 2022.

These are his opinions, not the opinions of his firm or clients, so don’t cite part of this post against him in an actual case. Every case is different, so don’t rely on this post as legal advice for your case.

[1] Motion Med. Tech., LLC v. Thermotek, Inc., 875 F.3d 765, 779-80 (5th Cir. 2017). The jury’s award of $6 million for unfair competition was reversed on other grounds.

[2] Id. at .

[3] Id. at 776-78.

[4] Id. at 780 (citing ERI Consulting Eng’rs, Inc. v. Swinnea, 318 S.W.3d 867, 879 (Tex. 2010)).

Comments:

Good examples. Accounting always a challenge in determining damages. As lawyers we need a regular dose of basic accounting and this article was right on point.

Thanks, Stanley